The decision on what technology to purchase next and when is a constant variable in the normal business cycle of any community banker.While there are certainly many different offerings you might want: online account opening and mobile services to account analysis and fraud detection, there are very few vendors to choose from and this is having a big impact on the cost of new services.

In fact, by any measure the Core IT and data processing market it is an oligopoly. 85% of services available to community banks are controlled by just three vendors: Fiserv, Fidelity and Jack Henry. When a vendor holds all the cards the price you pay can take many direct and indirect forms that are not always obvious to the buyer. In this article I hope to begin educating the banking executive about just how powerful and wily vendors can be in up-selling and cross-selling new services they know you need and only they posses.

What oligopolists know is that any of their products can be purchased with multiple forms of currency and to the extent they can manipulate them together into a “deal” the vendor will carry the day in any negotiation. Cash, trade, credits and time (contract extensions) are forms of currency and levers they play to create the appearance of an affordable offering at Fair Market Value (FMV). The concepts of trust, partnership and you’ve-got-nowhere-else-to-go are emotional factors they rely upon to obfuscate the real impact and close the deal. Since there are no CIOs running community banks these days vendors cunningly bank upon this general technology ignorance, authorizing service providers in getting away with the loot and not leaving a trace.

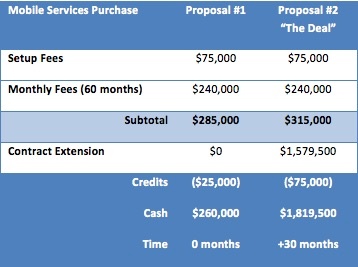

Consider the real life example of $400 Million asset ACME Bank in California that purchased Mobile Banking services with Vendor F in 2015. The proposal (#1) from Vendor F included a $75,000 setup fee and a monthly expense of $3,500 plus transaction fees based on volume. Without being asked, the vendor generously offered a $25,000 flex credit to be used against the $75,000 setup fee contingent upon the Bank signing by the end of April 2015 and implementing before EOY. A vendor investment summary calculated a total of $260,000 over the next 5 years not including variable volume transaction fees and annual increases. Few banks have any idea how many of their customers will adopt mobile or how quickly. While vendors possess this data nationally they rarely model these predictions within an investment summary so it remains an unknown variable and therefore not subject to the larger negotiation.

At the time of the proposal ACME Bank had about 30 months remaining on their data processing contract with Vendor F (exactly at the mid-way point of a 5-year deal) paying approximately $52,650 per month. After some analysis by the CFO the $50,000 cash outlay [$75,000 setup - $25,000 Flex Credit] plus the cost of business distraction, etc. is a lot of money when they are just barely into the black. After a review of the proposal and on the advice of their attorney the Bank asked that the setup fee be “…waived or financed into the deal somehow to lessen the blow.” Vendor F agreed and provided a counter proposal (#2) that included a larger $75,000 flex credit – effectively eliminating the setup costs – along with an increased monthly processing cost to $4,000 lowering the total 5-year investment to $240,000 ($20,000 less than proposal A). Sounds reasonable until you realize the devil is always...

The Bank verbally agreed to the ‘investment summary’ and requested a formal amendment. After reviewing the formal amendment it was noted that Vendor F had added a stipulation requiring the master agreement be extended by 30 months so that both the master and Mobile Services program would be coterminous. Salesperson for Vendor F advised the Bank that making both contracts coterminous would simplify vendor management and was their standard policy when providing such a large flex credit. How nice of them. To the CFO it seems a reasonable compromise. After all, the Bank had no intention of ever leaving Vendor F and extending the master now would clear his plate of a lengthily renegotiation in 2016. Kicking the can seemed to make sense and they signed the amendment.

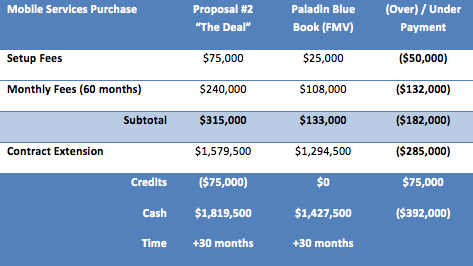

So let’s take a look at what really happened here. The vendor proposed a combination of credit and time extension to create the appearance of lowering the overall investment summary for the new product in exchange for simply extending their current agreements by 30 months at the same rate. A ‘win-win’ by any measure until you compare prices nationally to the Paladin Blue Book (PBB) and realize the following:

A) The original quoted setup fee was stated significantly above FMV and was never actually negotiated by the Banker. Remember, the vendor volunteered a 33% discount with proposal #1. This negotiation technique convinces the buyer that the seller is negotiating in good faith and doesn’t want to haggle. The actual setup fee per PBB for these same mobile service for Banks under $500 million is $20,000 to $25,000 (max).

B) The monthly fees stated in proposal #1 of $3,500 and proposal #2 of $4,500 were never negotiated by the Banker and both are above Fair Market Value. Remember the vendor traded away the $75,000 in setup fees for a $500 monthly increase (to $4,000) and a 30-month contract extension. The Banker trusted the vendor, didn’t ask for outside advice and would have never known they were agreeing to pay $2,200 too much per month! Paladin Blue Book price = $1,800 per month.

C) ACME Bank thought they were extending their fairly priced Core data processing contract for another 30 months, saving time and avoiding the need to write a $50,000 check today for mobile services setup. What they actually didn’t know is that their agreement could have been renewed and restructured (yes, even with 30 months remaining) lowering the current monthly cost from $52,650 to $43,150 – reduction of $9,500 per month! Not taking advantage of this opportunity cost the Bank another $285,000 (before growth or annual increases are factored in) by harmlessly agreeing to extend a mere 30 months.

So then, what did these mobile services actually cost ACME Bank?

While the actual names, location and identities of the Bank and Vendor shall remain anonymous and confidential – the demonstration is all too familiar. Did the vendor take advantage of the Banker and cross an ethical boundary by over-charging by $392,000? No. The Banker never got outside help; accessed a Blue Book or negotiated any of the details and therefore he deserved it. Buying critical services that are the lifeblood of your Bank from an oligopolist may be intimidating, daunting and certainly time consuming but that cannot be an excuse when the stakes are so high.

Many bankers would rather not risk the time doing something they are not really sure about (technology contract negotiation) or do anything to disturb the comfortable working relationship and trust they enjoy with their service provider partners. Bringing in an outside party to negotiate on your behalf seems it could disturb the marriage. I’ll conclude this article without leaning too hard on the common sense missing in this example but remind you to always Trust your Vendor – but Verify you are getting a good deal. Always. And finally, if you cannot get hold of your vendor account executive after signing a new agreement just remember that cell phones don’t work on cruise ships.

Contact Paladin today to get your free Core & IT reduction asessment!