Back in the 1980s, there were more banks, smaller banks, and little technology. We were still driving checks around, there was no online banking, and networked ATMs was the latest in bank technology. At the time, the rule of thumb for bankers was that each bank employee produced about $20,000 of operating profit per year. Since each bank had about 100 employees, operating profit was about $2mm per community bank. In this article, we look at how this equation has changed and what it means for the future.

Banking History and What Accounts for Banker Productivity

Run a regression on banker productivity and the two items that account for 94.4% of the result is business model and operating leverage. Back in the ’80s, as is true today, your business strategy largely accounted for your profitability. Back then, if you were a foreign bank whose parent company plopped down a couple hundred million dollars in deposits and liabilities and then threw ten to 15 people to watch over US investments your productivity was high to the order of about $1mm per employee.

Next, to foreign banks, trust banks were very productive, producing around $800k of operating profit per employee. By the mid-’80s, monoline banks started to hit their stride with their focus on credit card and captive finance. Technology such as the central core processors, ATM, and cash counters was all the rage. On average, each of these major pieces of technology took the place of 20+ workers at each bank.

By the late ’90s, names like Primerica, Household Bank, JC Penney, Greenwood, American Express, Sears, Monogram and Chemical not only were profitable but then were the first banks to start employing technology on a mass scale which could be highly leveraged.

During this time, larger regional banks such as Security Pacific out West, and Manufacturers Bank and Citibank out East started to leverage computers, email, and processing equipment in mass to spike banker productivity. By the early ’90s, community banks started to employee technology like desktop computers, sorters, and processing equipment to boost productivity.

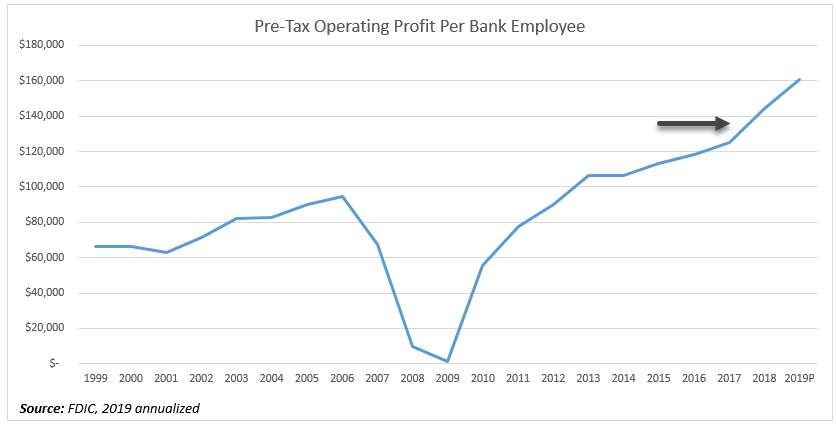

By 1999, the average banker produced $66,000 of operating profit. This continued until the peak of 2006 when check imaging became popular at which time the average banker produced $94,565 of operating profit per employee.

After the Great Recession, technology such as online and mobile banking started to change the game, and productivity jumped. By 2017, two things occurred. One was that banks started to reduce their branch footprint even more as a result of mobile banking. The other trend was data analytics was adopted on a widespread basis, and banks started to be more effective at marketing.

As a result of gaining operating leverage through technology, as of 2019, each banker produces about $160.729 of operating profit per year or eight times the profitability of a banker in the ’80s.

Lessons For Bankers

There are a couple of major insights that can be drawn from this data that is important to keep in mind during strategic planning:

Worker Displacement: For anyone scared that the next robot will replace the need for a branch teller or credit analyst, consider this fact. Technology has only reallocated the need for human capital and has not displaced it. In the 1980s, the banking industry employed roughly 1.5 million people. Before the recession, the industry employed its high-water mark of 2.2 million. In 2019, banks employ well over two million people with fintech-type banks employing another half million. While technology and the number of hired bankers are not correlated, profit is. In other words, if you are concerned with providing jobs to your community, the best way to do that is to employ technology, grow the bank, and increase worker productivity. If you think you are saving jobs by not employing technology, you are not.

Bank Disparity: To the point above, there is an increasing disparity among banks when it comes to worker productivity. In 2000, the average standard deviation of operating profit per full-time employee (FTE) was $200k, in 2019, that has increased to $243k. Now, it is not uncommon for a community bank with the right business model that aggressively employs technology can produce over $500k per employee (e.g., Silicon Valley Bank, Hingham Institution for Savings, etc.).

Leverage Not Size: For all those banks that complain that they are not large enough to afford technology, the data doesn’t bear that out. Banks of all sizes have successfully employed technology to boost productivity. Consider that JP Morgan Chase produces $172,421 of operating profit per employee, which is good but not great. PNC Bank only produces $102,389 of operating profit per employee, which is below average. Meanwhile, Bank 7 (OK) is $700mm in assets and does $365,097 of operating profit per employee leveraging their mobile and online technology. Complexity hurts productivity. What bankers want is to be able to leverage a single process utilizing technology.

Stop Traditional Thinking: It costs banks $1mm to automate loan production and $1mm to open a branch. In this day and age, most banks still do the latter because that is how they were taught. However, most banks over $700mm in total assets will break even on that loan production system within the first year. That branch, in this interest environment, you could be in 2027 before you see a profit.

Tight Margins Should Mean More Tech Investment: When the yield curve is flat, and margins compress, a bank can generate more profit from cost savings than from incremental lending or deposits. Next to credit risk, labor is the next largest input into a bank’s production of profit. Management should strive to constantly seek operating leverage, and that usually means making each banker more productive. Expanding mobile banking, card controls, digital account opening, and loan processing should be on every bank’s radar screen for this strategic planning session.

Choose Your Business Model Wisely: While you may not be able to turn yourself into a captive finance bank, it is likely that you can do a better job at focusing resources on a select number of products lines that you want to expand outside of your current footprint in order to create scale. Some banks that produce over $250k per FTE have done this with self-storage financing, dental practice banking, religious banking, and about 100 other ideas.

Putting This into Action

Making your human capital more productive is a consistent trend among banks and one that is now more important than ever. Managing technology is a Rubik’s Cube-type effort, and bankers have to be thinking several moves ahead to cover at least the next five years, if not ten. Some systems like mobile banking will take years to change out while other systems such as your core take five or more. The key for this year is to figure out what technology platforms can move the needle the most can either reduce cost and/or increase revenue the fastest. After that, figure out how you can use that technology to specialize in certain customer segments, and you can achieve scale at a faster rate. Banks that have done this have more than doubled their operating profit per employee.