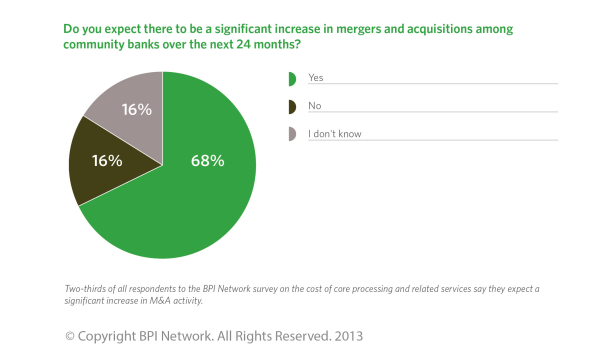

For an institution implementing a future merger strategy, what would another $250,000+ per year in additional profit mean (without having to make a single loan)?

A prominent senior analyst for a national investment banking firm recently asked the question "Would you replace your roof before you sold a home to increase the resale value or would you rather negotiate the credit back to the buyer for the repair during the purchase negotiation?" For most of us common sense would prevail and of course we would make the necessary improvements to an asset before we sold as a way to increase the equity and clear the decks for a simpler, more profitable negotiation. Getting your home ready for purchase is a best practice. So why then are bankers continuing to avoid this thinking when it comes time to sell or buy another institution? The answer is complex and at its center is a fundamental, entrenched cultural value of following old wisdom versus new. There remains hesitation to go outside the box and consider new ideas once thought taboo. Smart leaders are beginning to rethink M&A preparation in a totally different way for a new era in community banking and credit union history.

The facts are that most leaders today lack the previous professional experience of sitting at the helm when buying or selling an institution (less than 5% polled do). The last major contraction period was some 20 years ago and yet todays CEOs and CFOs follow the tablets brought down from the mountain without questioning the wisdom in the old M&A playbook. The tools available to increase shareholder and franchise value are gone. Net Interest Margin (NIM) is decreasing and guaratneed to compress further when rates begin to rise again. Non-Interest Income is rarely available if you intend to compete for customers against the larger regional and national banks. So then what's left? Cutting expenses, improving efficiency and lowering the barriers to exit for major 3rd party contracts. Fix the roof, paint the house, install insulation so the asset has greater value, looks better to your future merger partner and has stronger curb appeal. Institutions have to make money and improve shareholder equity on the expense side today and for the foreseeable future if buy or sell is a possibility.

Since 2009 you've cut all the major costs including facility, people, event travel and your golf game. But most community financial instutions surveyed in the Less Burn, More Return study [May 2013] are missing a huge opportunity by unknowingly refusing to 'restructure' or even 'touch' core and IT services contracts for fear the opposite impact is true. Arguably core and IT services (ie. Fiserv, Fidelity, Jack Henry, Harland, Intuit, Elan, etc.) are the second largest expense line item on any P&L. On average, institutions between $250M and $2 Billion are reducing these costs by $1.2 Million over five years without changing vendors. Old M&A preparation wisdom informs the leadership to not touch these contracts for fear the termination, conversion or longer term comittment will hurt shareholders in a buy or sell transaction when actually new wisdom informs us this can be incorrect thinking. But you have to look to find out!

One CEO interviewed in the study renewed a 7 year deal with Fiserv just 15 months before selling his $350 Million asset bank. Because they lowered the costs by over $1.4 Million and improved the vendor separation clauses he estimated it added 7% to the shareholder benefit and saved the instituiton over $700,000 in termination expense. Adding immediate profit to the bottom line (about $18,000 per month) for a continuous 15 months permitted a much lower burn rate projection in the purchase negotiation and helped to orchestrate a higher valuation. Since termination clauses are typically tied to monthly expense, the reduction had a double-dip effect and saved the shareholders the huge pain of a $700K cram down.

For those institutions potentially buying, the changes that can be made to vendor contracts are numerous and available for the asking (assuming you know what to ask for). However, few of these provisions exist by default in these agreements because afterall the vendor wrote the contract - not the banker. There is not a single vendor-issued agreement on the planet that benefits your shareholders in either a buy or sell opportunity and so you have to make your moves before an announced acquisition. Once the vendor knows you need their help to buy or sell your franchise - they're going to make it very expensive to swallow and this is why deals are falling apart in due dilligence. The old rules no longer apply. It's a different world and these vendors swing far more weight in your buy/sell transaction than they did 20 years ago. Unfortunately, few of the lawywers and investment bankers that are by your side during the due diligence and purchase negotiations phase know much about what to do with these specific core and IT vendor issues and by then, it's usually too late.

New wisdom begins with being proactive and pulling these contracts off the shelf and studying them with a third party that knows what they're doing and before you start dancing to buy or sell.