Let me tell you about one of the worst trading days of my life.

On October 29, 2025, I watched $70,000 of my Fiserv stock evaporate as the company lost $30 billion in market cap—a 44% plunge. Don't tell me how much further it fell the rest of the week—I didn't look!

But here's the thing: I wasn't surprised.

Neither were thousands of community bank and credit union leaders. We've been watching this train wreck in slow motion since First Data bought Fiserv in 2019. Wall Street just finally noticed what community bankers have been living with: Fiserv treating its clients like captive ATMs while underinvesting in critical services.

What Actually Happened

Fiserv's Q3 2025 earnings revealed:

- Organic revenue growth crashed from 16% (2024) to 1% (Q3 2025)

- Guidance slashed from 10-12% to 3.5-4%

- Adjusted EPS down 11%

- Free cash flow cut to $4.25B from $5.5B

CEO Mike Lyons admitted on the call:

"Decisions to defer certain investments and cut certain costs improved margins in the short term, but are now limiting our ability to serve clients in a world-class way."

Translation: They cut corners, pocketed the savings, and now they can't deliver.

"Fiserv's recent results have increasingly relied on short-term initiatives... placing too much emphasis on in-quarter results versus building long-term relationships."

Decoded: Gaming quarterly earnings instead of serving banking clients.

The Argentina Illusion

Strip away Argentina's hyperinflation windfall, and Fiserv's "growth story" collapses faster than a house of cards in a dust storm.

Argentina contributed 5 points to 2023's 12% growth, 10 points to 2024's 16% growth, and 2 points to 2025's 5% growth.

Do the math: Without Argentina, Fiserv's core U.S. business grew 6%, 6%, and 3% over three years. That's not a growth company. That's a utility slowly dying—like a buggy whip maker after Henry Ford showed up.

Mid-single digits for a "technology" company. That dog won't hunt.

Schedule a confidential review of your Fiserv situation with Paladin fs → Here

The Real Story Wall Street Just Discovered

Wall Street is shocked. We're not. We've been riding this rodeo for years, watching Fiserv mistreat clients with one-sided, overpriced deals for antique software.

Fiserv invests only 6-8% of free cash flow in innovation. Real tech companies invest 18-22%. Apple, Microsoft, Amazon and Google spend nearly three - four times what Fiserv does on R&D. Why? Oligopoly. When you control the market with Jack Henry and FIS, you just collect rent.

Their flagship products—Premier, DNA, Signature—were invented in the 1980s-90s. Sure, they've added API layers that monetize Fintech innovations, but the core architecture is decades old. Lipstick on a pig.

At September's Omaha P3 Conference, 50%+ of Premier clients (banks over $1B) weren't using Fiserv's digital banking. A decade ago? 90% adoption. Now? Under 50%. That's not market evolution. That's client abandonment. A stampede from a burning barn.

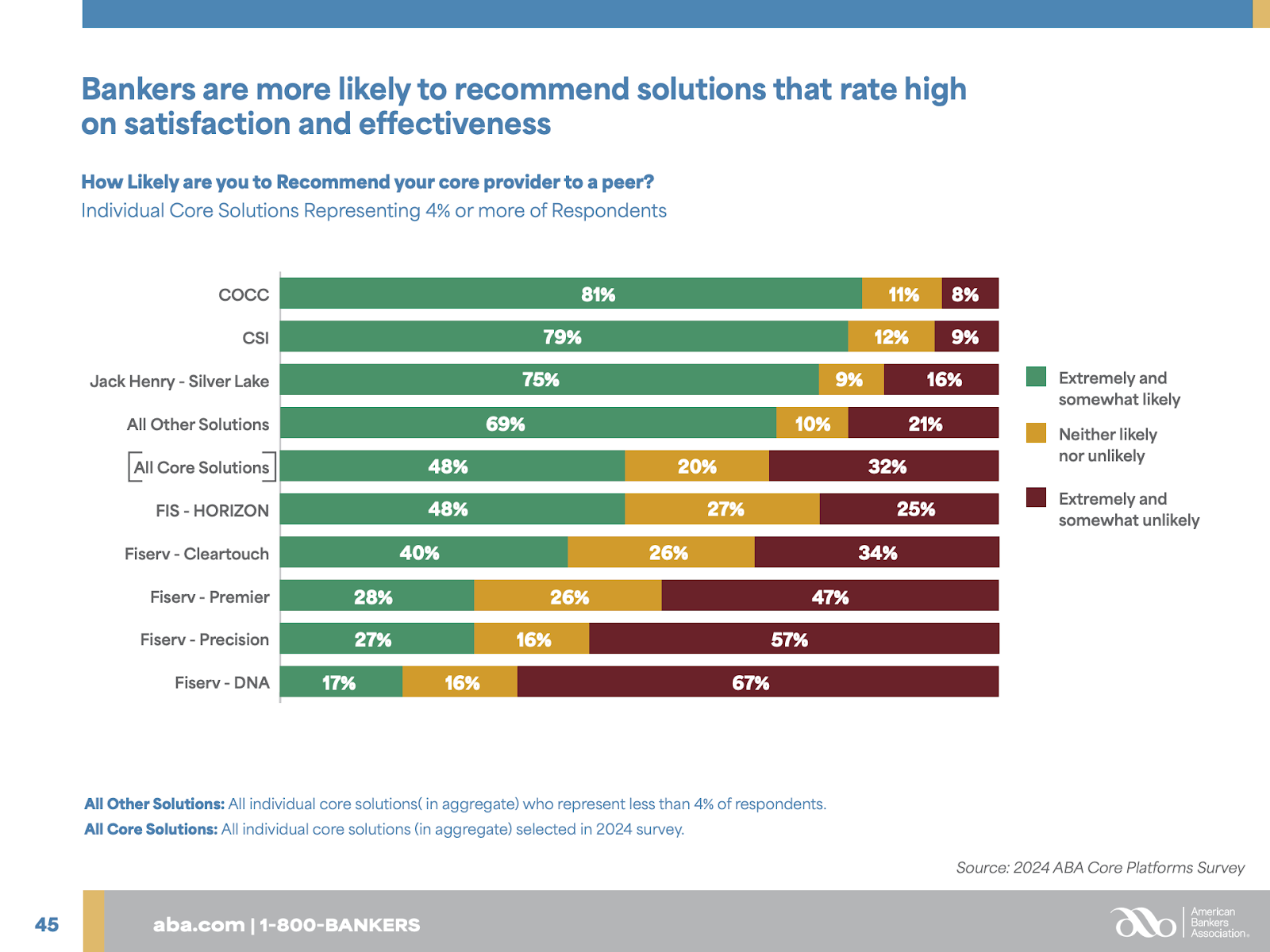

And here's the kicker: About a year ago, the American Bankers Association released their annual satisfaction survey of core banking providers. Want to guess where Fiserv ranked? Dead last. Bottom of the barrel. The worst-rated core provider among community banks and credit unions. Not exactly a ringing endorsement from the people who actually have to use their systems every day.

Service levels have "dropped precipitously by their own admission." Implementation delays. Buggy releases. Support tickets closed for no reason.

While our business model focuses on helping banks get better deals with their incumbent suppliers - avoiding the pain and suffering that comes along with a core conversion - Paladin has helped more banks leave Fiserv in the last 5 years than the previous 15 years combined. That's an exodus.

The Five Critical Risks Fiserv Clients Must Address NOW

If you're running a community bank or credit union on Fiserv infrastructure, you're facing five existential risks.

Risk #1: The Great Core Consolidation Gamble

Fiserv announced they're reducing 16 core platforms to 5, expecting 1,400+ clients to migrate to CoreAdvance by 2028.

My question: How in the hell are they going to pull this off?

They just admitted to years of underinvestment and service gaps. They've got a revolving door in the C-suite. They're under margin pressure. And now they're executing the most complex technical migrations in community banking history?

Partner, this is like herding 1,400 cats through a thunderstorm while riding a unicycle. Blindfolded.

What happens when banks want to leave during this chaos? Will Fiserv have resources for clean de-conversions? Or will banks be trapped in conversion bottlenecks?

Is this a roadmap or a road trip to nowhere?

Risk #2: Leadership Chaos

Complete C-suite and board refresh: New CEO, CFO, two Co-Presidents, Board Chairman, Audit Chair, and Board Member—all during massive operational transformation, margin compression, client erosion, 16-to-5 core consolidation, and service recovery.

The truth: Roadmap commitments were made by people who no longer work there. Who's accountable now?

Risk #3: Price Increases Coming

Fiserv is "deprioritizing short-term revenue initiatives"—killing revenue streams that subsidized your pricing.

They mentioned "elimination of certain fees." Where will they make up the shortfall? You.

Expect price increases disguised as "value-based adjustments" or "inflationary pass-throughs." Expect mandatory bundles. Expect creative contract reinterpretations.

Without protections—cost caps, CPI-based increases, itemized schedules—you're exposed. Fiserv needs to restore margins.

Risk #4: Service Level Deterioration by Design

Lyons was brutally honest: "Decisions to defer certain investments and cut certain costs improved margins in the short term, but are now limiting our ability to serve clients in a world-class way."

Translation:

- Understaffed implementation teams = delayed go-lives

- Deferred innovation = buggy releases

- Cut support staff = unanswered tickets

- Postponed infrastructure upgrades = system outages

The problem: Most Fiserv contracts don't have real Service Level Agreements (SLAs). They have SLOs—Service Level Objectives.

SLAs have teeth. SLOs are suggestions.

An SLA says: "Miss 99.9% uptime three months running, you can terminate without penalty and we'll refund last quarter's fees."

An SLO says: "We'll try really hard to hit 99.9% uptime, but if we don't, we'll try harder next time. Call us and register a ticket—we'll call you back. Eventually. Maybe."

Guess which one Fiserv uses?

You're paying premium prices for degrading service with zero recourse. That's like paying for steak and getting hamburger. And when you complain, they tell you they'll "work on it."

Risk #5: M&A Transaction Penalties

Fiserv acts as a silent shareholder in every merger. They didn't help find the target, fund the deal, or do due diligence. But they'll extract millions through termination fees, de-conversion costs, forced upgrades, and per-item charges (six or seven figures).

The irony: Fiserv gains market share at zero acquisition cost while you pay. It's like charging a rancher every time he adds cattle—except the rancher doesn't own the cattle. You do.

Without M&A protections, your next acquisition could cost millions in unnecessary penalties.

The Opportunity

Most consultants would tell you to jump ship. I'm not.

This moment of Fiserv instability is your greatest leverage point in years.

When vendors are vulnerable, they negotiate. When they need to prove client retention to Wall Street, they'll work deals they wouldn't touch six months ago.

Smart institutions are:

- Renegotiating NOW (24-30 months before renewal, not 18 months out)

- Hardening contracts with real SLAs, cost caps, M&A protections, flexible exits

- Benchmarking pricing against real market data (not Fiserv's claims)

- Evaluating alternatives with unbiased intelligence

- Building optionality with 'off ramps' and 'carve outs'

What Paladin Does Differently

No sales pitch. Just facts:

18 years. Only this. We don't sell software or get kickbacks. We negotiate technology contracts for community banks and credit unions ($50M-$30B assets). Gunslingers, not snake oil salesmen.

We have the data. Our Paladin Blue Book contains proprietary benchmark pricing on every major vendor. We know exactly what your peers pay.

"Posse" approach. You get a team of experts in core systems, digital banking, payments, and contract law.

Free research first. We'll tell you if we can deliver value you couldn't achieve alone. If we can't, we'll say so.

Lifetime Contract Protection Services (LCPS). We guarantee you'll never overpay for the life of the term we negotiate.

DIY options:

- PaladinQuoteCheck.com: Upload quotes for instant market comparison

- LoneRanger.com: For $1M+ negotiations, get red-lined contracts, benchmarks, masterclass, and six months of coaching

- BankTechOracle.ai: AI-powered contract risk analysis (first in America).

Your Move

Fiserv is not going out of business. They're generating $4.5B in free cash flow with a $40B market cap. They have thousands of captive clients and operate in an oligopoly.

But execution risk is real. They're attempting to rope and brand 1,400 banks while short-staffed, under-resourced, with an entirely new management team.

The next 5-7 years will be make-or-break.

Three options:

- Staying? Harden your contract, right-price services, build exit optionality.

- Evaluating alternatives? We'll show you what's possible with unbiased research.

- Not sure? Start with free research. We'll tell you if we can help before you spend a dime.

You can't do nothing.

Don't wait for renewal panic. Don't hope Fiserv figures it out. Don't assume your contract protects you.

Use Fiserv's weakness as your strength.

Vendors who lost $30B yesterday will negotiate today. Question is: Will you have the data, expertise, and leverage to get the deal you deserve?

Ready to protect your institution? Let's talk about strategy.

Schedule a confidential review of your Fiserv situation with Paladin fs → Here

Aaron M. Silva is the CEO of Paladin fs, a technology contract negotiation and consulting firm that has served community banks and credit unions exclusively for 18 years. Paladin has helped hundreds of institutions restructure vendor agreements, saving clients millions while ensuring they never overpay for critical technology services.